- FeaturesFeaturesHow it WorksUnderstand the MaxiFi features that help you build your lifetime planRoth Conversion OptimizerMaxiFi helps you optimize conversions and reduce taxesUse CasesHow can you put MaxiFi to use?Life Insurance Contingency PlanningGet peace of mind from life insurance recommendations tailored for youLiving Standard Monte CarloManage your living standard risk with confidence

FeaturesHow it Works . Understand the MaxiFi features that help you build your lifetime planLearn More

FeaturesHow it Works . Understand the MaxiFi features that help you build your lifetime planLearn More - ServicesServicesOverviewChoose the right level of support for your plan and needsFlight CheckGet off the ground with comprehensive, expert guidanceCo-PilotElevate your financial plan with one of MaxiFi’s certified financial plannersConcierge ServicesPersonal, expert guidance to make the most of your financial plan

.png)

- Resources

- Why MaxiFiMaxiFiEconomics-Based PlanningHow Nobel Prize-winning economics gives you a clear view of your financesCase StudiesReal stories about how MaxiFi helps users make smarter decisionsTestimonialsMaxiFi is trusted by households and experts for clarity and confidenceHow MaxiFi ComparesWith so many tools out there, how do you know MaxiFi is right for you?PressRead expert commentary and critical acclaim for MaxiFi

.webp)

- Pricing

- AboutCompanyOur VisionThe best person to take control of your financial futureMedia ResourcesLogos, background information, and media contactsFounder and AdvisorsMeet Laurence Kotlikoff and the visionary MaxiFi teamAffiliate ProgramAs a MaxiFi affiliate, you can share offers and discountsCareersWhy working at MaxiFi is rewarding, empowering, and impactfulContactQuestions or feedback? Get in touch with the MaxiFi team

.webp)

.png)

How MaxiFi Helps You Plan Your Financial Future

MaxiFi software incorporates all your financial data, helping you create a highly detailed lifetime financial plan.

Plan with Confidence, Understand Your Context

From sustainable spending and tax optimization to risk assessment and key life decisions, MaxiFi empowers youto make smarter, more informed financial choices for a secure future.

Find a Lifetime Spending Level You Can Afford

See the affordable spending level you can sustain for life based on your current and expected resources.

Maximize Your Financial Resources

Optimize your plan to see how you can get the most out of Social Security and your retirement accounts, including Roth conversions.

Comprehensive Tax and Benefit Calculations

Incorporates detailed Federal, State and FICA tax calculations as well as Social Security benefits and Medicare Part B premiums.

A Clear View of Your Risk

Powerful Living Standard Monte Carlo ® allows you to assess risk and reward of different investment strategies and spending behavior.

Savings and Insurance Plan

Provides a savings and life insurance coverage plan for protecting and maintaining your affordable spending level.

Confidence for Life’s Key Decisions

Provides insight into career choices, housing decisions, retirement planning and other financial decisions at any age and stage.

.webp)

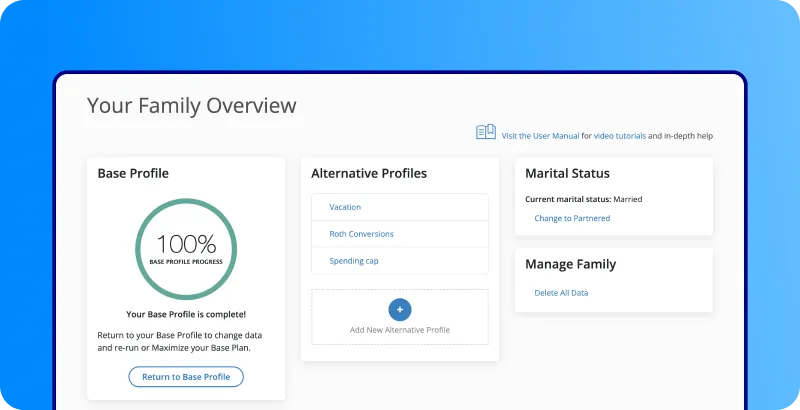

A complete lifetime roadmap for your income, spending, savings and life insurance needs

To get started, all you need to do is input your data and MaxiFi will calculate your Base Plan—a complete lifetime roadmap for your income, spending, savings and life insurance needs.

Your Base Plan is dynamic, so you can return at any time to update with new information, new expectations, or to see how your plan is impacted when trying to make life-changing decisions—whether to take a new job, when to buy a new home—or everyday decisions like how much to budget for groceries or entertainment.

Clear Inputs for a Clear Financial Plan

Building your base plan is easy, takes minutes, and only requires minimal data entry. Just start with:

Your current and expected earnings

Balances for your savings, checking, investment, and retirement accounts

Expected contributions to retirement accounts from you and your employer

Account balances and expected withdrawals for 529 Education Savings Accounts

Your pensions

Social Security covered earnings and current benefits (if any)

Any expenses on your primary and vacation homes (rent, mortgage, condo fees, etc.)

Your real estate holdings, receipts, and expenses

Other expected major expenses or receipts

Detailed, dynamic, and comprehensive reports

Make informed decisions with easy-to-use, pre-built reports that show you:

A Lifetime Balance Sheet with your Projected Lifetime Resources and Projected Lifetime Spending

Annual income

Annual spending—fixed and discretionary

Annual suggested savings and withdrawals from non-retirement accounts (stocks, bonds, mutual funds)

Annual suggested withdrawals from retirement accounts

Annual cash flow for income for each spouse if married

Annual household net worth

Annual taxes – Federal, State and FICA

Annual Social Security benefits

And when circumstances change? Adjust and re-run your plan as often as you like, giving you all the information and control you need to create and manage your plan.

Working with a planner? No problem, export your report as a PDF or Excel file to share with your financial planner.

.webp)

Maximize your Base Plan and build strategies to safely raise your affordable spending level

Once you’ve created your Base Plan, MaxiFi's optimization engine can analyze thousands of scenarios to find ways to safely raise your annual discretionary spending—potentially increasing it by hundreds of thousands of dollars over your lifetime.

Finds the best Social Security filing strategy to get the highest benefits for you and your spouse

Calculates tax efficient retirement account withdrawal start dates

Shows tax efficient Roth versus non-Roth withdrawals

Optimizes Roth conversions (MaxiFi Premium and MaxiFiPRO Only)

.webp)

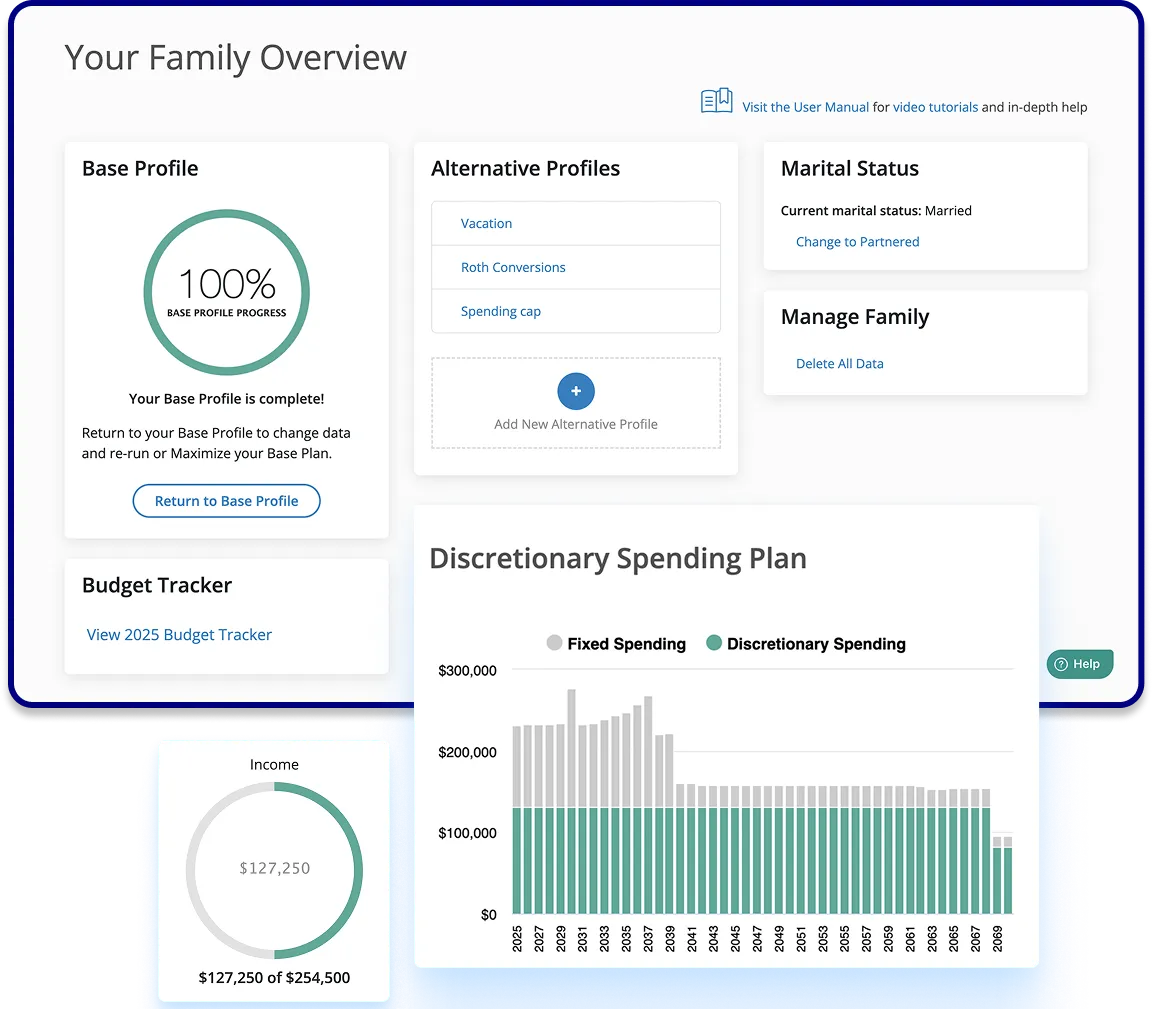

Know exactly where you stand on your spending and saving targets

When you're happy with your Base Plan, create a budget for the year with a few clicks. MaxiFi's Budget Tracker tool helps you keep on track to meet the key spending and savings numbers in your plan. It also allows you to make sure your income expectations for the year match your actual income.

Set and update income, fixed spending, and savings targets for the year automatically from your Base Plan

Create spending target categories based on a typical household budget or create your own

Easily view and update your progress throughout the year at any time from any device

Export your budget and your transactions data to Excel at any time

Manage your living standard risk

MaxiFi's Living Standard Monte Carlo® simulations show how different investment strategies and spending behaviors impact your bottom line – your living standard.

MaxiFi has two ways to run Living Standard Monte Carlo to help you balance living standard risk and return:

Upside Investing

Input current and future stock investments and when you'll exit the market. The software finds your base living standard floor assuming all other investments are safe and your stocks lose all value. As you exit the market, MaxiFi raises your living standard floor based on the simulated amount of stocks that have been converted to safe assets.

.webp)

Full Risk Investing

Full risk investing assumes you spend each year from both your safe and risky assets. You tell MaxiFi how you will invest through time and how aggressively you'll spend. This results in a plan with more spending in early years based on the presumption your risky assets will pay off.

Learn More: How Living Standard Monte Carlo® Works

.webp)

Optimize Roth conversions to maximize your living standard

Roth conversions involve the transfer of retirement assets from a traditional retirement account, such as a 401(k) or SIMPLE IRA, into a Roth account. While the account owner pays income tax on the converted assets, future earnings and withdrawals from the Roth account can be made tax free.

Determining when to convert assets to Roth accounts and how much to convert in each year is an extremely complex problem. While other tools may be able to simply optimize for minimized taxes, MaxiFi is the only software that finds the annual conversion amounts that maximize your lifetime discretionary spending or estate. It takes into consideration all these factors:

How Roth conversions affect current and future taxes

Required minimum distributions (RMDs) from non-Roth retirement accounts

Taxes on Social Security benefits

Medicare Part B IRMAA premiums

Cash-flow constraints

Your willingness to accept a lower living standard in the short term in order to enjoy a higher living standard in the long term

Income streams from financial assets, Social Security, pensions, and annuities

Your assumed rate of return on regular assets and retirement accounts

Your assumed future inflation rate

Your household’s demographic composition

Learn more about how it works, or read our case study

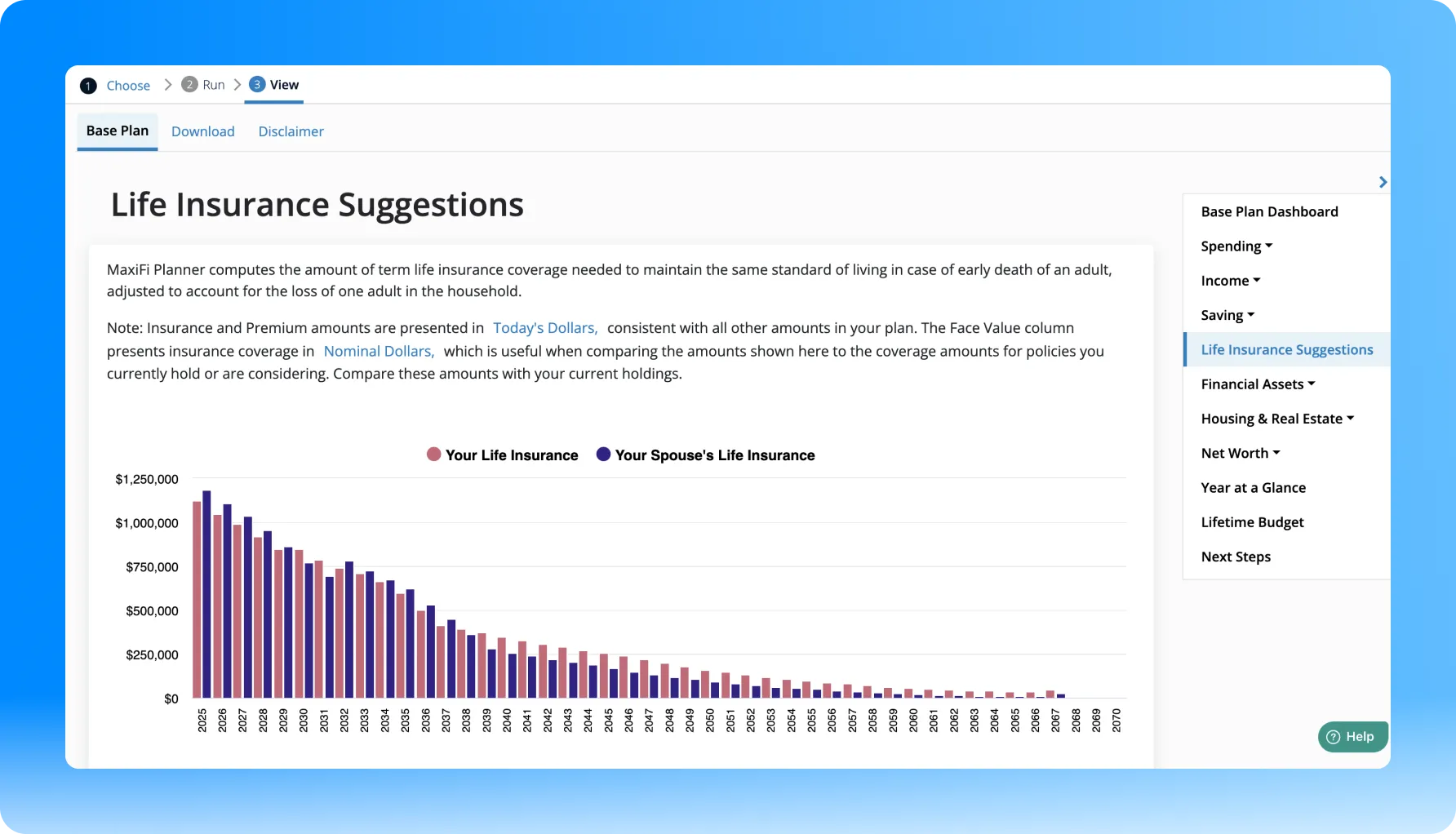

Precise life insurance calculations for maximum peace of mind

MaxiFi's standard life insurance calculations are already extremely powerful. It's the only software that determines how much coverage your family needs each year to maintain your current living standard if you or your spouse were to pass away.

But what if you plan to downsize your home if that happens? In this case, life insurance needs will be overstated because selling your home will result in additional resources for you and other survivors. This is where MaxiFi's Life Insurance Contingency Planning feature comes into play.

Available in MaxiFi Premium, contingency planning allows you to enter changes if you or your spouse die early. Enter contingencies for Housing, Future Earnings, Special Receipts, Special Expenses, and Retirement Account Contributions, customized based on your personal circumstances and choices.

MaxiFi accounts for these changes and ensures that your life insurance coverage amounts accurately consider your new financial situation while maintaining your household's current living standard.

Learn more about how it works

MaxiFi puts the most powerful, accurate financial planning approach into your hands

Based on years of research and fine-tuning, MaxiFi makes highly detailed annual Federal and State tax calculations and considers the full range of Social Security benefits.

If it could affect your future living standard, then we think the software you use should show you how. That’s why MaxiFi gives you control over dozens of settings so you can model different maximum ages, inflation rates, changes to Social Security benefits or tax rates, and many others.

Tax Considerations

Fully updated with One Big Beautiful Bill Act (OBBBA) of 2025 tax changes

Includes SECURE Act 2020 rules for Required Minimum Withdraws

Shows tax efficient Roth versus non-Roth withdrawals

Federal income taxes

FICA taxes

Pensions

State income taxes

The Alternative Minimum Tax

Itemization decision

Tax credits

Deductions and exemptions

Capital gains and dividends

State-specific schedules

Social Security benefit taxation

Federal bracket indexation

Capital gains on home sales

Municipal bond preference

Self-employment tax

Social Security Benefits

Retirement Insurance Benefits

Spouse’s Insurance Benefits

Divorced Spouse’s Insurance Benefits

Social Security Disability Insurance Benefits

Child In-Care Spouse’s Insurance Benefits

Widow(er)’s Insurance Benefits

Divorced Widow(er)’s Insurance Benefits

Child’s Insurance Benefits

Childhood Disability Benefits

Surviving Child’s Insurance Benefits

Father’s and Mother’s Insurance Benefits

Social Security Rules and Provisions

New Social Security laws and grandfathering rules

Early benefit reductions

Delayed retirement credits

The earnings test

Adjustment of the reduction factor

Re-computation of benefits

Option to suspend and reinstate retirement benefits

Family maximum

Combined family maximum

Disabled family benefit maximum

RIB LIM on widow(er) benefits when deceased spouse claimed early

Restricted application and deeming rules

Alternate widow(er)’s benefits when the deceased spouse died before age 62