- FeaturesFeaturesHow it WorksUnderstand the MaxiFi features that help you build your lifetime planRoth Conversion OptimizerMaxiFi helps you optimize conversions and reduce taxesUse CasesHow can you put MaxiFi to use?Life Insurance Contingency PlanningGet peace of mind from life insurance recommendations tailored for youLiving Standard Monte CarloManage your living standard risk with confidence

FeaturesHow it Works . Understand the MaxiFi features that help you build your lifetime planLearn More

FeaturesHow it Works . Understand the MaxiFi features that help you build your lifetime planLearn More - ServicesServicesOverviewChoose the right level of support for your plan and needsFlight CheckGet off the ground with comprehensive, expert guidanceCo-PilotElevate your financial plan with one of MaxiFi’s certified financial plannersConcierge ServicesPersonal, expert guidance to make the most of your financial plan

.png)

- Resources

- Why MaxiFiMaxiFiEconomics-Based PlanningHow Nobel Prize-winning economics gives you a clear view of your financesCase StudiesReal stories about how MaxiFi helps users make smarter decisionsTestimonialsMaxiFi is trusted by households and experts for clarity and confidenceHow MaxiFi ComparesWith so many tools out there, how do you know MaxiFi is right for you?PressRead expert commentary and critical acclaim for MaxiFi

.webp)

- Pricing

- AboutCompanyOur VisionThe best person to take control of your financial futureMedia ResourcesLogos, background information, and media contactsFounder and AdvisorsMeet Laurence Kotlikoff and the visionary MaxiFi teamAffiliate ProgramAs a MaxiFi affiliate, you can share offers and discountsCareersWhy working at MaxiFi is rewarding, empowering, and impactfulContactQuestions or feedback? Get in touch with the MaxiFi team

.webp)

.png)

Are You Making the Right Roth Conversion Moves?

.png)

.png)

.png)

.png)

Roth Conversions are Complex. MaxiFi’s Roth Conversion Optimizer ™ Makes Them Easy

Convert with Precision

End the Guesswork

Gain Financial Confidence

The most powerful personal financial planning engine.

Don’t just take our word for it.

.webp)

Customers love our software

"As a Certified Financial Planner, I use MaxiFi when I am completing my client's overall financial plan. I continually hear that my clients love... being able to understand what their discretionary spending can look like in today's dollars projected for the rest of their life. MaxiFi also makes it super easy to update the projections on an annual basis. The ease to create multiple scenarios to determine the best accounts to hold investments and to determine the ideal Roth conversion strategy to build the highest lifetime discretionary spending tops my list of features available."

"I believe my husband and I will enjoy a much better retirement without worry because of this program. If we should both live long lives, I can easily see... that... will gain tens of thousands of dollars in income over the course of our retirement by applying just one or two maximization principles. And even in the short term, we should be able to spend more in early retirement than I had thought possible and still remain secure in our old age. Thank you so much for designing this excellent program!"

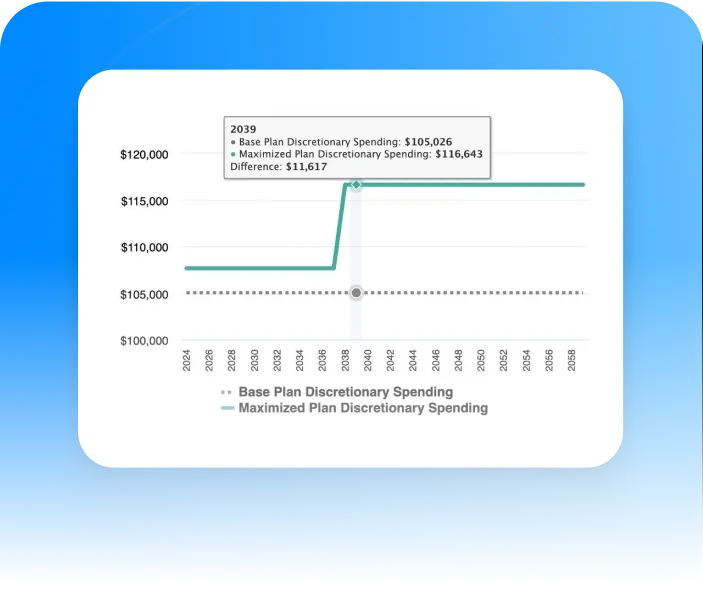

"I want to commend the team for introducing the Roth Conversion Optimization module. It's a game-changer. Previously, I would spend... running dozens of model iterations, manually adjusting Roth conversion amounts to find the optimal strategy. I even created a basic Excel model using Solver, but it lacked MaxiFi's accuracy, particularly in areas like tax bracket and IRMAA changes over time. The results speak for themselves: my new MaxiFi-optimized plan increases my lifetime discretionary spending by over $100,000. This more than justifies my subscription fees for years to come! I should also mention that a few years ago, I paid a Certified Financial Planner over $5,000 to provide an optimized conversion strategy. MaxiFi's strategy is far superior. Thank you all for your excellent work!"

"Thanks for creating this Roth Conversion feature. Generally Roth Conversion advice is that they are no-brainers for some, and for others... and always ending with the comment these are complicated and a suggestion to be sure to consult with tax and financial experts. That's not been helpful. However, MaxiFi's Roth Conversion Optimizer makes it simple. It takes all the income and portfolio changes into account and lays out the plan for not just the current year - but the future years. It certainly gave me peace with a sophisticated calculation instead of my own personal modeling in a simple spreadsheet. Thanks, MaxiFi!"

Take Control of Your Retirement With MaxiFi’s Roth Conversion Optimizer™

Maximize Your Savings

.webp)

Run Multiple Scenarios

.webp)

Apply the Plan

CEO, Maxifi

Backed by Economic

Research and Insights

MaxiFi’s Roth Conversion Optimizer™

A Breakthrough by Laurence Kotlikoff

Featured in

.png)

.png)

.png)

.png)

Frequently asked questions

What are Roth Conversions and How Do They Work?

Roth conversions let you transfer assets from regular IRAs, 401(k)s, and 403(b)s to their Roth counterparts. These conversions are taxable. But Roth assets grow tax free and aren’t taxed on withdrawal. Plus, Roth withdrawals do not trigger Social Security benefit taxation or Medicare Part B IRMAA taxation. Roth conversions also limit tax uncertainty, reduce future Required Minimum Distributions (RMDs), and facilitate tax-advantaged bequests of Roth balances. MaxiFi’s Roth Conversion Optimizer calculates how much to convert annually based on precise projections of federal and state income taxes, taxes on Social Security benefits, Medicare IRMAA taxes, and RMDs.

What Should You Consider When Planning Roth Conversions?

Converting more this year means higher current, but lower future taxes. Current conversions also impact gains from future conversions. Thus, an optimal conversion strategy requires simultaneously deciding how much to convert this year and in all future years. Moreover, conversions can change taxes abruptly by putting you in higher or lower federal-income, state-income, and IRMAA tax brackets as well as alter the taxation of Social Security benefits. In short, federal income taxes are only part of the picture and converting only when federal income tax brackets are low is rarely optimal. Remarkably, making large-scale conversions early on, even at the cost of paying federal income taxes at the highest rate, may produce major future tax savings by dramatically lowering future brackets.

What Factors Influence the Timing and Amount of Roth Conversions?

With optimal Roth conversions, one size fits none. Your age, spouse’s age (if married), longevity, wages, retirement dates, Social Security collection strategy, and levels of regular and retirement assets all matter. So do future tax changes, your Roth withdrawal strategy, and the state income taxes you’ll face in retirement. Finally, paying higher immediate taxes can cause cash-flow problems limiting the conversions you can sustain.

How Do Roth Conversions Affect Financial Consistency Over Time?

Reducing lifetime taxes via Roth conversions permits higher lifetime spending with the timing of increased spending depending on cash-flow constraints. But a household’s spending path affects its current and future asset accumulation which then affects taxable asset income and taxes. Thus, Roth conversions impact taxes, which impact spending, which impact taxes, and on and on. Mathematically, optimal Roth conversion is a highly non-linear, simultaneous equations problem requiring MaxiFi’s advanced algorithms to get right.

Should Everyone Pursue Large-Scale Roth Conversions?

Each household’s optimal conversion strategy is unique and for some, Roth conversions may not help. But applying MaxiFi’s Roth Conversion Optimizer to a range of alternative test cases produces surprising findings. For many households, early conversion of all or virtually all regular IRAs, Roth-convertible 401(k)s and 403(b)s, as well as other tax-deferred assets is the winning strategy. Yes, doing so means far higher tax brackets early on. Yet, the tax reductions from much lower future taxes can produce, on balance, lower lifetime taxes. Converting on a large scale can make these tax reductions substantial.

Where Can I See Examples of How Roth Conversions Work?

Check out our detailed Roth Conversion Optimizer case study on our website. It walks you through real-world scenarios showing the substantial tax savings and increased retirement spending achievable through strategic Roth conversions.

Will MaxiFi Help with Other Financial Decisions Beyond Roth Conversions?

Absolutely, the Roth optimizer is just one feature of the comprehensive MaxiFi software. When you purchase MaxiFi, you gain access to a versatile tool designed to assist you in making informed financial decisions throughout different stages of life. Whether you are far from retirement or already retired, MaxiFi lets you experiment with various life scenarios and compare their impacts on your living standard. Here’s how MaxiFi can help you manage a wide range of financial decisions:

• For those not near retirement:

• Taking a new job

• Having a child

• Buying a home

• Moving to a different state

• Paying off student loans

• Deciding how much to spend and save each year

• Determining the right amount of life insurance

• For those nearing retirement:

• Deciding when you can afford to retire

• Choosing the best time to apply for Social Security benefits

• Determining when to start taking withdrawals

• Exploring whether to reduce to part-time work before retiring

• Evaluating whether to move or downsize your home

• Deciding whether to sell assets before retirement

• For retirees:

• Downsizing your home

• Purchasing long-term care insurance

• Postponing Social Security benefits

• Continuing to buy life insurance

• Paying off your mortgage

• Exploring different investment and spending strategies

• Adjusting retirement account withdrawals

• Supporting a child or grandchild's education or other needs

• Changing the order of withdrawal from retirement accounts

• Moving to a different state

• Annuitizing parts of your 401(k)

By investing in MaxiFi software, you can evaluate these and other financial decisions, clearly seeing how each choice might affect your financial future and optimize your strategy accordingly.

Other Financial Planning Tools are Free, Why Should I Pay for MaxiFi Software?

Most other financial planning software companies have other ways of making money, usually by managing and investing your assets or selling you financial products such as life insurance. Our sole focus is developing personal financial planning software to provide you with a solid, detailed financial plan you can trust. The free tools also use simplistic, outdated "rules of thumb" and lack precision when it comes to crucial aspects of your plan, such as Social Security benefits and state taxes. Because our focus is on planning, we constantly work to improve the power and accuracy of our software. At Economic Security Planning, Inc., we don’t sell, recommend, or advertise any financial products, nor recommend particular financial advisors. This allows us to focus strictly on providing the best financial suggestions.